Upcoming Event

Free Newsletter

Free Newsletter

Equity valuation conundrum

How do we reconcile the damage to the real economy with the stunning resilience of equities in 2020?

Tim Keating //December 23, 2020//

Equity valuation conundrum

How do we reconcile the damage to the real economy with the stunning resilience of equities in 2020?

Tim Keating //December 23, 2020//

“Everything in valuation gets back to interest rates.” —Warren Buffett

How do we reconcile the damage to the real economy with the stunning resilience of equities in 2020? The answer is near-zero interest rates.

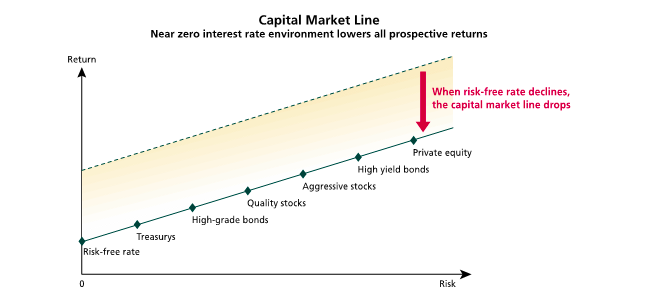

Let’s start with the capital market line, which establishes an equilibrium relationship between expected return and expected risk, and starting with the risk-free rate. Finance theory tells us that as we move to the right on the horizontal risk axis, the corresponding expected return on the vertical axis must also increase, resulting in an upward-sloping line.

In response to the onset of the pandemic in March, the Fed preemptively lowered short-term interest rates to near zero. This drove down the anchor point of the capital market line and simultaneously lowered the prospective returns of all asset classes.

Equity Valuation 101

Relative to any single metric, most measures of equity valuations today are considerably higher than historical averages. But this is a one-factor analysis in a two-factor equation. There is a crucial variable missing: interest rates.

The current value, or price, of an asset is the discounted value of expected future cash flows. When interest rates are lowered, the discounted value of the future cash flows increases, and vice versa.

Investors in equities have historically demanded an equity premium of 350 basis points above the 10-year Treasury note yield as compensation for volatility. If the 10-year Treasury yields 3%, the corresponding equilibrium earnings yield of equities would be 6.5% Since the earnings yield is the inverse of the price-to-earnings ratio, the implied P/E ratio in this example is 15.4x [1/6.5%]. In fact, this has roughly been the S&P 500’s average P/E multiple since World War II.

Fast forward to today, with the 10-year Treasury rate hovering just under 1%. When we add 350 basis points, the new prospective equilibrium earnings yield is 4.5% and the new corresponding “fair” P/E ratio spikes to 22.2x. Irrespective of any accretion to enterprise earnings that may be the result of a lower cost of debt capital, all else being equal, dropping interest rates by 2 percentage points causes a 44% increase in equity valuation multiples.

Conversely, a 2-percentage point increase in a hypothetical 10-year Treasury yield from 3% to 5% would demand a new earnings yield of 8.5%, and a corresponding fair of P/E of 12x, resulting in a multiple contraction of 22% from the original starting point of 15.4x.

The tech stock dilemma

The challenge when looking at the S&P 500 through a single valuation lens is that the index composition is far from homogenous. Today, there are two distinct groups of stocks in the S&P 500: tech and everything else.

The five largest tech companies (Apple, Microsoft, Amazon, Alphabet and Facebook) represent roughly 25% of the index’s market capitalization (up from 14% for the five biggest stocks in the index three years ago). As a group, these companies are growing rapidly and have demonstrated their ability to increase revenues and profit margins. Deservedly, they also have much higher P/E multiples and have accounted for nearly all the return in the market in 2020.

But these higher tech multiples are already fully baked into the index cake, and for the equity index investor the point becomes moot because, by design, it’s a package deal. The remaining companies in the index are slower growing, already enjoy maximum margins, have lower multiples, and have contributed comparatively little in terms of overall stock return.

This bifurcation in growth, valuation and performance makes it increasingly difficult to draw broad conclusions about a unitary “stock market.” But what’s the alternative to stocks? As Howard Marks notes in his “Coming into Focus” memo (Oct. 13, 2020):

Most decisions in investing are relative decisions. Investors try to find the most attractive opportunity to be able to achieve the highest risk-adjusted return…. Thus, assets and asset classes are inherently interconnected. Money moves from one asset class to the next in search of the best bargains, which get bought up until they’re at equilibrium with everything else. Changing the risk-free rate has the potential to reset the returns on everything [emphasis added].

The problem with bonds

As of Nov. 30, 2020, the yields on the 30-day T-bill (cash) and the 10-year Treasury (bonds) were 0.08% and 0.85%, respectively. After the Fed cut interest rates to near zero, accounting for inflation meant investors could expect to lose money holding U.S. Treasurys to maturity.

Moreover, Treasurys don’t have much room left for upside. If the 10-year’s yield dropped to zero, its market value would still rise by only about 8%.

In contrast, there could be plenty of downside. Consider a situation where the Fed keeps short-term rates near zero—as it has pledged to do through at least the end of 2022—but the yield curve steepens. If the yield on the 10-year Treasury rose to 2.5%, the note would lose about 15% of its value.

No alternative to equities

How can we reconcile the returns of stocks in 2020 with all the damage to the real economy, including earnings? Quite simply, there is no alternative to equities. Let’s begin with a few current equity valuation fundamentals.

- On Nov. 30, 2020, the S&P 500 closed at 3,621.63.

- As of Nov. 30, the consensus 12-month forward earnings estimate for the S&P 500 is about $166.

- Based on this estimate, the forward 12-month P/E ratio for the S&P 500 is 21.8x, and the corresponding earnings yield is 4.6%.

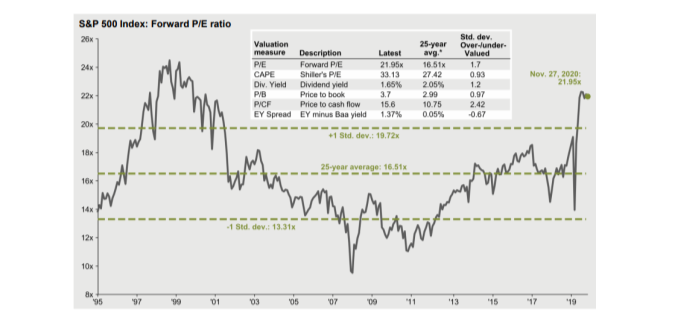

- The accompanying chart from J.P. Morgan Asset Management illustrates that the current forward P/E multiple is about 1.7 standard deviations above the 25-year average of 16.5x.

- The other equity valuation measures in the inset table (Shiller’s CAPE ratio, dividend yield, price-to-book and price-to-cash flow) all indicate overvaluation relative to the historic 25-year averages.

But take a close look at the “EY Spread.” This is the difference between the S&P 500 earnings yield and the yield on investment grade corporate bonds (as measured by the Moody’s Baa bond yield). Historically, these yields have traded at near parity (0.05% average). Yet today, the earnings yield is 1.4 percentage points above the corporate bond yield of 3.2%—equivalent to a relative undervaluation of equities by about a half a standard deviation.

Looking at a hypothetically fully recovered economy in 2022, the consensus earnings estimate rises 18% to $196, which drops the 2022 forward P/E multiple to 18.5x, the corresponding earnings yield to 5.4%, and the advantage over corporate bonds to 2.2%.

These earnings yield to bond yield comparisons ignore the extra 1.7% dividend yield that S&P 500 index investors receive.

In the current rate environment, asset prices are higher and prospective returns are likely lower. But decisions in investing are always relative. Inflation-adjusted yields on cash and bonds are negative. Notwithstanding sky-high P/E multiples in a handful of tech stocks, in this near-zero interest rate environment, there is no alternative to equities as an asset class for building and maintaining wealth.

Behavioral takeaway

Narrow framing involves making decisions without considering all the implications. In a financial context, it means evaluating too few factors regarding an investment. Regardless of the methodology used for valuing equities, there is always some measure or stream of cash flows—such as dividends or earnings—that must be discounted by some interest rate. In its simplest form, it’s a two-factor model. Valuing equities solely relative to a historical average ignores the variable of interest rates. Such narrowly framed thinking has caused many investors to make costly errors by shunning equities.