Upcoming Event

Free Newsletter

Free Newsletter

Roth IRA Conversion: 2020’s Unique Opportunity

With tax hikes possibly on the horizon, here’s one thing you can do now

Tim Keating //June 16, 2020//

Roth IRA Conversion: 2020’s Unique Opportunity

With tax hikes possibly on the horizon, here’s one thing you can do now

Tim Keating //June 16, 2020//

In response to the coronavirus pandemic, the federal government has already authorized about $3.6 trillion in new spending since late March—a number so enormous that it requires some context. As a reference point, total federal outlays for all of 2019 were about $4.4 trillion. The stimulus spending could grow even larger as unemployment rates reach above 20%, second only to the 25% level during the Great Depression.

And then there’s the federal debt. The U.S. government is on track to borrow about $4.5 trillion in the current fiscal year, more than triple last year’s $1.3 trillion. This debt level exceeds 100% of our GDP, the highest since the end of World War II. This explosion in federal debt raises a few obvious questions, among them how and when this spending will be paid for. It’s hardly a stretch to imagine that tax hikes might be on the horizon.

To hedge against potentially higher personal tax rates in the future, there is something you can do now: Convert some or all of a regular IRA[1] to a Roth IRA—provided you can afford to pay the associated taxes out of your nonretirement accounts. This simple financial planning move could significantly decrease your future tax burden and reduce complexities for your heirs.

If you meet one or more of these criteria, consider a Roth conversion in 2020:

- Your IRA balance is over $500,000.

- You are over age 70½ (or turned 72 in 2020), and do not have to take your required minimum distribution (RMD) in 2020.

- You expect your 2020 taxable income to be lower than your 2019 taxable income.

- You are in the 24% or 32% tax bracket.

- You can pay the taxes on a Roth conversion from your nonretirement assets.

Deferring income through retirement accounts

In addition to saving for retirement, retirement plan savers get to defer income until future years when they may be in a lower tax bracket. The two most common deferral vehicles are IRAs and employer-sponsored 401(k) plans.[2] While IRA distributions are taxed upon withdrawal, prior to 2020, you were able to delay distributions for significant periods, with the following effects:

- Although an IRA owner must take RMDs starting at age 70½, these distributions could be spread over the owner’s life expectancy.

- Upon the owner’s death, the surviving spouse could inherit the IRA and take distributions over his or her life expectancy.

- After the owner’s and surviving spouse’s death, the nonspousal beneficiaries (typically, the owner’s children and grandchildren) could take distributions over their life expectancies under a “stretch” IRA.

SECURE Act of 2019

In part to curb these long deferral periods, Congress passed the SECURE Act in December 2019.[3] While the new rules still allow surviving spouses to take distributions from an inherited IRA over their life expectancies, children and grandchildren named as successor beneficiaries, with limited exceptions, can no longer stretch distributions over their lifetimes. Now, 100% of an inherited IRA must be distributed to the heirs within 10 years of the owner’s or surviving spouse’s death.

Considering these new rules and the increased likelihood of higher tax rates in the future, now is an opportune time to review your tax and estate planning and potentially take action.[4]

Window of opportunity

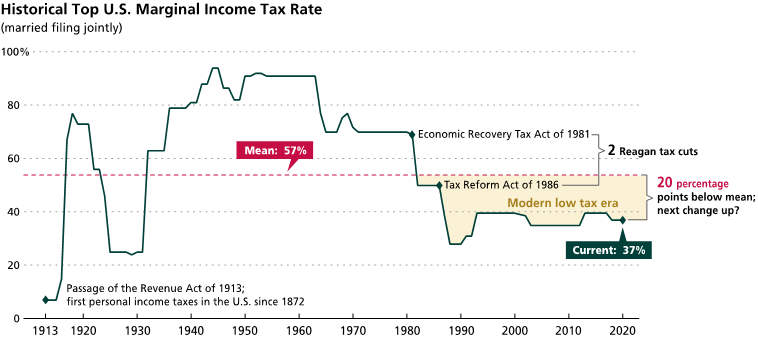

You might be surprised to learn that the current top marginal tax rate of 37% is in the lowest quarter for the 100-plus-year period since the passage of the Revenue Act of 1913, with a mean and median top marginal tax rate of 57% and 63%, respectively.

With the prospect of higher taxes and the elimination of the stretch IRA, now may be a once-in-a-lifetime chance to create a tax-efficient Roth nest egg. Regardless of your age or income, you can take steps to reduce future taxes by converting your current IRA into a Roth IRA, and you can even make multiple conversions over several years. The cost of conversion is the tax you must pay on the converted amount in the year of conversion.

Why pay taxes now on a Roth conversion rather than letting your IRA continue to grow tax-deferred for years to come?

- Distributions from a Roth IRA are 100% tax-free, meaning the appreciation on your Roth assets is never subject to income taxes.[5]

- Owners of Roth IRAs and their surviving spouses are never required to take distributions during their lifetimes. Thus, if you have other assets to fund your retirement years, your Roth IRA can continue to appreciate tax-free until it passes to your children or grandchildren tax-free.

- Although an inherited Roth IRA must be fully withdrawn by your children or grandchildren within 10 years of your or your surviving spouse’s death, there are some other important differences between IRAs and Roth IRAs. Your heirs will need to be vigilant tax planners if they inherit an IRA, since they will typically need to make withdrawals during the first nine years to avoid a large tax bill in the 10th year. Also, IRA withdrawals are taxed at the rates in effect in the year of withdrawal, which could be higher than today’s rates. Tax planning is much simpler for Roth beneficiaries since all withdrawals are tax-free. So while Roth withdrawals can be made in the first nine years, if your heirs don’t need the money, they would likely want to delay withdrawals until the end of the 10th year to allow the Roth account to grow tax-free as long as possible.

- Your tax adviser can help you minimize taxes upon conversion by “bracket-topping,” where you convert enough of your IRA to go to the edge of your existing tax bracket—or, if you feel strongly about higher future tax rates, even the next bracket. For example, in 2020, a married couple with $180,000 in taxable income is in the 24% marginal rate bracket, which starts at $171,051 and caps out at $326,600. In this case, the owner could convert up to $146,600 into a Roth IRA without moving to the next bracket, which is 32%.

Since you cannot roll over RMDs into a Roth IRA, you must first withdraw and pay taxes on your RMD before you can convert amounts from your IRA to a Roth IRA. But there is some good news for those who are currently taking RMDs: The CARES Act, passed in response to the coronavirus pandemic, suspended RMDs for 2020. Thus, IRA owners who do not need current retirement income may consider a Roth conversion in lieu of their 2020 RMDs.

Before completing a Roth conversion, which is irrevocable, you also need to assess any impact that this incremental income will have on certain tax phase-out rules, net investment income tax, and Medicare Part B and D premiums.

When our republic was in its infancy, Benjamin Franklin reminded us that nothing is certain but death and taxes. It now appears that higher taxes in the future may be getting closer to a certainty. Undoubtedly, Franklin would have encouraged us to plan wisely for the future.