Free Newsletter

Free Newsletter

Report: Small business profits decline as fuel costs rise and payroll growth slows

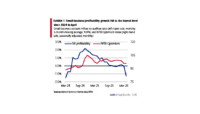

Bank of America reports small business profits fell 1.3% as fuel costs surged and payroll growth slowed, impacting sectors like transportation and agriculture.

Rising fuel costs and uncertainty pressure small businesses in the US, report says

Small businesses face rising fuel costs and increased uncertainty, impacting sectors like agriculture and transportation, according to Bank of America and NFIB data.

Report: Small business profits rise as technology spending grows in February

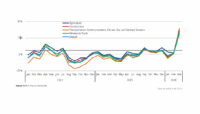

Bank of America reports small business profits rose 1.2% in February with a 14% increase in technology spending, signaling productivity focus amid cost pressures.

Women to Watch: Bank of America

An estimated $124tn will shift hands by 2048, with women set to inherit the majority—reshaping wealth, influence, and financial planning in America.

Government agency drops lawsuit against banks over Zelle fraud

The Consumer Financial Protection Bureau is dropping its lawsuit against the company that runs the Zelle payment platform and three U.S. banks as federal agencies continue to pull back on previous enforcement actions now that President Donald Trump is back in office.

Why The Consumer Plays An Important Role In Supporting Black Business Growth in Colorado

While August was Black Business Month, consumers can recognize and renew the role they play in supporting Black-owned businesses at any time of the year. There has been growth in overall […]

Women to Watch 2023 — Bank of America

Everywhere in Colorado, women are leading our business communities to new levels of success. They each have a unique story that has shaped our state through economic, social and enterprising […]

Surviving Food Inflation — How Colorado Restaurants Adapt to Rising Costs and Labor Challenges

Like countless other industries, the restaurant industry has been completely redefined by the pandemic. Restaurant owners felt optimistic about the post-COVID world but were immediately presented with a continued headline […]

GUEST COLUMN — President of Bank of America and DDP on the Power of Economic Diversification

Downtown Denver has positioned itself for continuous growth and success despite the challenges and changes stemming from a post-pandemic environment. Denver ranked sixth for the fastest-growing city in the US […]

4 Ways to Offer Wellness Tools and Retain Your Workforce

As labor shortages continue to impact companies across industries, businesses are shifting their focus to employee retention. According to Bank of America‘s recent Workplace Benefits Report, 46% of employers have seen […]

The internship that is preparing students to change the world

If you or someone you know wants to make a difference, you can learn more and apply online at www.bankofamerica.com/studentleaders